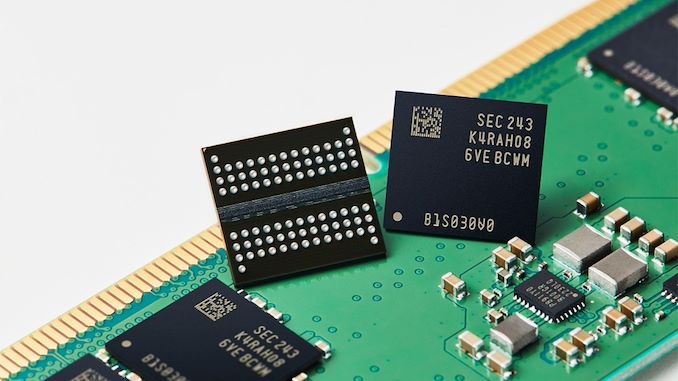

Following the magnitude 7.2 earthquake that struck Taiwan on April 3, 2024, there was immediate concern over what impact this could have on chip production within the country. Even for a well-prepared country like Taiwan, the tremor was the strongest quake to hit the region in 25 years, making it no small matter. But, according to research compiled by TrendForce, the impact on the production of DRAM will not be significant. The market tracking company believes that Taiwanese DRAM industry has remained largely unaffected, primarily due to their robust earthquake preparedness measures.

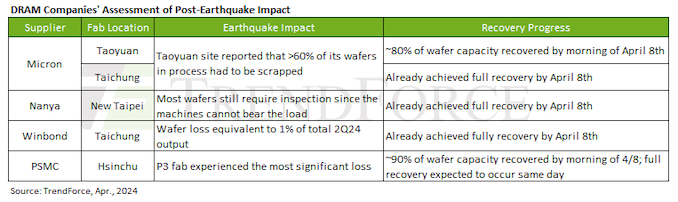

There are four memory makers in Taiwan: Micron, the sole member of the "big three" memory manufacturers on the island, runs two fabs. Meanwhile among the smaller players is Nanya (which has one fab), Winbond (which makes specialty memory at one fab), and PSMC (which produces specialty memory at one plant). The study found that these DRAM producers quickly resumed full operations, but had to throw away some wafers. The earthquake is estimated to have a minor effect on Q2 DRAM production, with a negligible 1% impact, TrendForce claims

In fact, as Micron is ramping up production of DRAM on its 1alpha and 1beta nm process technologies, it increases bit production of memory, which will positively affect supply of commodity DRAM in Q2 2025.

Following the earthquake, there was a temporary halt in quotations for both the contract and spot DRAM markets. However, the spot market quotations have already largely resumed, while contract prices have not fully restarted. Notably, Micron and Samsung ceased issuing quotes for mobile DRAM immediately after the earthquake, with no updates provided as of April 8th. In contrast, SK hynix resumed quotations for smartphone customers on the day of the earthquake and proposed more moderate price adjustments for Q2 mobile DRAM.

TrendForce anticipates a seasonal contract price increase for Q2 mobile DRAM of between 3% and 8%. This moderate increase is partly due to SK hynix's more restrained pricing strategy, which is likely to influence overall pricing strategies across the industry. The earthquake's impact on server DRAM primarily affected Micron's advanced fabrication nodes, potentially leading to a rise in final sale prices for Micron's server DRAM, according to TrendForce. However, the exact direction of future prices remains to be seen.

Meanwhile, DRAM fabs outside of Taiwan have none been directly affected by the quake. This includes Micron's HBM production line in Hiroshima, Japan, and Samsung's and SK hynix's HBM lines in South Korea, all of which are apparently operating with business as usual.

In general, the DRAM industry has shown resilience in the face of the earthquake, with minimal disruptions and a quick recovery. The abundant inventory levels for DDR4 and DDR5, coupled with weak demand, suggest that any slight price elevations caused by the earthquake are expected to normalize quickly. The only potential outlier here is DDR3, which is nearing the end of its commercial lifetime and production is already decreasing.

Memory

Demand for high-performance processors for AI training is skyrocketing, and consequently so is the demand for the components that go into these processors. So much so that SK hynix this week is very publicly announcing that the company's high-bandwidth memory (HBM) production capacity has already sold out for the rest of 2024, and even most of 2025 has already sold out as well.

SK hynix currently produces various types of HBM memory for customers like Amazon, AMD, Facebook, Google (Broadcom), Intel, Microsoft, and, of course, NVIDIA. The latter is an especially prolific consumer of HBM3 and HBM3E memory for its H100/H200/GH200 accelerators, as NVIDIA is also working to fill what remains an insatiable (and unmet) demand for its accelerators.

As a result, HBM memory orders, which are already placed months in advance, are now backlogging well into 2025 as chip vendors look to secure supplies of the memory stacks critical to their success.

This has made SK hynix the secnd HBM memory vendor in recent months to announce that they've sold out into 2025, following an earlier announcement from Micron regarding its HBM3E production. But of the two announcements, SK hynix's is arguably the most significant yet, as the South Korean firm's HBM production capacity is far greater than Micron's. So while things were merely "interesting" with the smallest of the Big Three memory manufacturers being sold out into 2025, things are taking a more concerning (and constrained) outlook now that SK hynix is as well.

SK hynix currently controls roughly 46% - 49% of HBM market, and its share is not expected to drop significantly in 2025, according to market tracking firm TrendForce. By contrast, Micron's share on HBM memory market is between 4% and 6%. Since HBM supply of both companies is sold out through the most of 2025, we're likely looking at a scenario where over 50% of the industry's total HBM3/HBM3E supply for the coming quarters is already sold out.

This leaves Samsung as the only member of the group not to comment on HBM demand so far. Though with memory being a highly fungible commodity product, it would be surprising if Samsung wasn't facing similar demand. And, ultimately, all of this is pointing towards the indusry entering an HBM3 memory shortage.

Separately, SK hynix said that it is sampling 12-Hi 36GB HBM3E stacks with customers and will begin volume shipments in the third quarter.

Memory

Demand for high-performance processors for AI training is skyrocketing, and consequently so is the demand for the components that go into these processors. So much so that SK hynix this week is very publicly announcing that the company's high-bandwidth memory (HBM) production capacity has already sold out for the rest of 2024, and even most of 2025 has already sold out as well.

SK hynix currently produces various types of HBM memory for customers like Amazon, AMD, Facebook, Google (Broadcom), Intel, Microsoft, and, of course, NVIDIA. The latter is an especially prolific consumer of HBM3 and HBM3E memory for its H100/H200/GH200 accelerators, as NVIDIA is also working to fill what remains an insatiable (and unmet) demand for its accelerators.

As a result, HBM memory orders, which are already placed months in advance, are now backlogging well into 2025 as chip vendors look to secure supplies of the memory stacks critical to their success.

This has made SK hynix the secnd HBM memory vendor in recent months to announce that they've sold out into 2025, following an earlier announcement from Micron regarding its HBM3E production. But of the two announcements, SK hynix's is arguably the most significant yet, as the South Korean firm's HBM production capacity is far greater than Micron's. So while things were merely "interesting" with the smallest of the Big Three memory manufacturers being sold out into 2025, things are taking a more concerning (and constrained) outlook now that SK hynix is as well.

SK hynix currently controls roughly 46% - 49% of HBM market, and its share is not expected to drop significantly in 2025, according to market tracking firm TrendForce. By contrast, Micron's share on HBM memory market is between 4% and 6%. Since HBM supply of both companies is sold out through the most of 2025, we're likely looking at a scenario where over 50% of the industry's total HBM3/HBM3E supply for the coming quarters is already sold out.

This leaves Samsung as the only member of the group not to comment on HBM demand so far. Though with memory being a highly fungible commodity product, it would be surprising if Samsung wasn't facing similar demand. And, ultimately, all of this is pointing towards the indusry entering an HBM3 memory shortage.

Separately, SK hynix said that it is sampling 12-Hi 36GB HBM3E stacks with customers and will begin volume shipments in the third quarter.

Memory

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's.

Demand for high-performance processors for AI training is skyrocketing, and consequently so is the demand for the components that go into these processors. So much so that SK hynix this week is very publicly announcing that the company's high-bandwidth memory (HBM) production capacity has already sold out for the rest of 2024, and even most of 2025 has already sold out as well.

SK hynix currently produces various types of HBM memory for customers like Amazon, AMD, Facebook, Google (Broadcom), Intel, Microsoft, and, of course, NVIDIA. The latter is an especially prolific consumer of HBM3 and HBM3E memory for its H100/H200/GH200 accelerators, as NVIDIA is also working to fill what remains an insatiable (and unmet) demand for its accelerators.

As a result, HBM memory orders, which are already placed months in advance, are now backlogging well into 2025 as chip vendors look to secure supplies of the memory stacks critical to their success.

This has made SK hynix the secnd HBM memory vendor in recent months to announce that they've sold out into 2025, following an earlier announcement from Micron regarding its HBM3E production. But of the two announcements, SK hynix's is arguably the most significant yet, as the South Korean firm's HBM production capacity is far greater than Micron's. So while things were merely "interesting" with the smallest of the Big Three memory manufacturers being sold out into 2025, things are taking a more concerning (and constrained) outlook now that SK hynix is as well.

SK hynix currently controls roughly 46% - 49% of HBM market, and its share is not expected to drop significantly in 2025, according to market tracking firm TrendForce. By contrast, Micron's share on HBM memory market is between 4% and 6%. Since HBM supply of both companies is sold out through the most of 2025, we're likely looking at a scenario where over 50% of the industry's total HBM3/HBM3E supply for the coming quarters is already sold out.

This leaves Samsung as the only member of the group not to comment on HBM demand so far. Though with memory being a highly fungible commodity product, it would be surprising if Samsung wasn't facing similar demand. And, ultimately, all of this is pointing towards the indusry entering an HBM3 memory shortage.

Separately, SK hynix said that it is sampling 12-Hi 36GB HBM3E stacks with customers and will begin volume shipments in the third quarter.

Memory

, Winbond (which makes specialty memory at one fab), and PSMC (which produces specialty memory at one plant). The study found that these DRAM producers quickly resumed full operations, but had to throw away some wafers. The earthquake is estimated to have a minor effect on Q2 DRAM production, with a negligible 1% impact, TrendForce claims</p>

<p>In fact, as Micron is ramping up production of DRAM on its 1alpha and 1beta nm process technologies, it increases bit production of memory, which will positively affect supply of commodity DRAM in Q2 2025.</p>

<p style="text-align: center;"><a href="https://www.anandtech.com/show/21344/impact-of-earthquake-on-dram-output-in-q2-negligible-analysts"><img alt="" src="https://images.anandtech.com/doci/21344/20240410_143442_2024-04-10_143205_575px.png" /></a></p>

<p>Following the earthquake, there was a temporary halt in quotations for both the contract and spot DRAM markets. However, the spot market quotations have already largely resumed, while contract prices have not fully restarted. Notably, Micron and Samsung ceased issuing quotes for mobile DRAM immediately after the earthquake, with no updates provided as of April 8th. In contrast, SK hynix resumed quotations for smartphone customers on the day of the earthquake and proposed more moderate price adjustments for Q2 mobile DRAM.</p>

<p>TrendForce anticipates a seasonal contract price increase for Q2 mobile DRAM of between 3% and 8%. This moderate increase is partly due to SK hynix's more restrained pricing strategy, which is likely to influence overall pricing strategies across the industry. The earthquake's impact on server DRAM primarily affected Micron's advanced fabrication nodes, potentially leading to a rise in final sale prices for Micron's server DRAM, according to TrendForce. However, the exact direction of future prices remains to be seen.</p>

<p>Meanwhile, DRAM fabs outside of Taiwan have none been directly affected by the quake. This includes Micron's HBM production line in Hiroshima, Japan, and Samsung's and SK hynix's HBM lines in South Korea, all of which are apparently operating with business as usual.</p>

<p>In general, the DRAM industry has shown resilience in the face of the earthquake, with minimal disruptions and a quick recovery. The abundant inventory levels for DDR4 and DDR5, coupled with weak demand, suggest that any slight price elevations caused by the earthquake are expected to normalize quickly. The only potential outlier here is DDR3, which is nearing the end of its commercial lifetime and production is already decreasing.</p>

</p> Memory){kind=link}

, Winbond (which makes specialty memory at one fab), and PSMC (which produces specialty memory at one plant). The study found that these DRAM producers quickly resumed full operations, but had to throw away some wafers. The earthquake is estimated to have a minor effect on Q2 DRAM production, with a negligible 1% impact, TrendForce claims</p>

<p>In fact, as Micron is ramping up production of DRAM on its 1alpha and 1beta nm process technologies, it increases bit production of memory, which will positively affect supply of commodity DRAM in Q2 2025.</p>

<p style="text-align: center;"><a href="https://www.anandtech.com/show/21344/impact-of-earthquake-on-dram-output-in-q2-negligible-analysts"><img alt="" src="https://images.anandtech.com/doci/21344/20240410_143442_2024-04-10_143205_575px.png" /></a></p>

<p>Following the earthquake, there was a temporary halt in quotations for both the contract and spot DRAM markets. However, the spot market quotations have already largely resumed, while contract prices have not fully restarted. Notably, Micron and Samsung ceased issuing quotes for mobile DRAM immediately after the earthquake, with no updates provided as of April 8th. In contrast, SK hynix resumed quotations for smartphone customers on the day of the earthquake and proposed more moderate price adjustments for Q2 mobile DRAM.</p>

<p>TrendForce anticipates a seasonal contract price increase for Q2 mobile DRAM of between 3% and 8%. This moderate increase is partly due to SK hynix's more restrained pricing strategy, which is likely to influence overall pricing strategies across the industry. The earthquake's impact on server DRAM primarily affected Micron's advanced fabrication nodes, potentially leading to a rise in final sale prices for Micron's server DRAM, according to TrendForce. However, the exact direction of future prices remains to be seen.</p>

<p>Meanwhile, DRAM fabs outside of Taiwan have none been directly affected by the quake. This includes Micron's HBM production line in Hiroshima, Japan, and Samsung's and SK hynix's HBM lines in South Korea, all of which are apparently operating with business as usual.</p>

<p>In general, the DRAM industry has shown resilience in the face of the earthquake, with minimal disruptions and a quick recovery. The abundant inventory levels for DDR4 and DDR5, coupled with weak demand, suggest that any slight price elevations caused by the earthquake are expected to normalize quickly. The only potential outlier here is DDR3, which is nearing the end of its commercial lifetime and production is already decreasing.</p>

</p> Memory){kind=link}

, Winbond (which makes specialty memory at one fab), and PSMC (which produces specialty memory at one plant). The study found that these DRAM producers quickly resumed full operations, but had to throw away some wafers. The earthquake is estimated to have a minor effect on Q2 DRAM production, with a negligible 1% impact, TrendForce claims</p>

<p>In fact, as Micron is ramping up production of DRAM on its 1alpha and 1beta nm process technologies, it increases bit production of memory, which will positively affect supply of commodity DRAM in Q2 2025.</p>

<p style="text-align: center;"><a href="https://www.anandtech.com/show/21344/impact-of-earthquake-on-dram-output-in-q2-negligible-analysts"><img alt="" src="https://images.anandtech.com/doci/21344/20240410_143442_2024-04-10_143205_575px.png" /></a></p>

<p>Following the earthquake, there was a temporary halt in quotations for both the contract and spot DRAM markets. However, the spot market quotations have already largely resumed, while contract prices have not fully restarted. Notably, Micron and Samsung ceased issuing quotes for mobile DRAM immediately after the earthquake, with no updates provided as of April 8th. In contrast, SK hynix resumed quotations for smartphone customers on the day of the earthquake and proposed more moderate price adjustments for Q2 mobile DRAM.</p>

<p>TrendForce anticipates a seasonal contract price increase for Q2 mobile DRAM of between 3% and 8%. This moderate increase is partly due to SK hynix's more restrained pricing strategy, which is likely to influence overall pricing strategies across the industry. The earthquake's impact on server DRAM primarily affected Micron's advanced fabrication nodes, potentially leading to a rise in final sale prices for Micron's server DRAM, according to TrendForce. However, the exact direction of future prices remains to be seen.</p>

<p>Meanwhile, DRAM fabs outside of Taiwan have none been directly affected by the quake. This includes Micron's HBM production line in Hiroshima, Japan, and Samsung's and SK hynix's HBM lines in South Korea, all of which are apparently operating with business as usual.</p>

<p>In general, the DRAM industry has shown resilience in the face of the earthquake, with minimal disruptions and a quick recovery. The abundant inventory levels for DDR4 and DDR5, coupled with weak demand, suggest that any slight price elevations caused by the earthquake are expected to normalize quickly. The only potential outlier here is DDR3, which is nearing the end of its commercial lifetime and production is already decreasing.</p>

</p> Memory | https://compbuddey.blogspot.com/2024/04/report-impact-of-taiwanese-earthquake.html){kind=link}

, Winbond (which makes specialty memory at one fab), and PSMC (which produces specialty memory at one plant). The study found that these DRAM producers quickly resumed full operations, but had to throw away some wafers. The earthquake is estimated to have a minor effect on Q2 DRAM production, with a negligible 1% impact, TrendForce claims</p>

<p>In fact, as Micron is ramping up production of DRAM on its 1alpha and 1beta nm process technologies, it increases bit production of memory, which will positively affect supply of commodity DRAM in Q2 2025.</p>

<p style="text-align: center;"><a href="https://www.anandtech.com/show/21344/impact-of-earthquake-on-dram-output-in-q2-negligible-analysts"><img alt="" src="https://images.anandtech.com/doci/21344/20240410_143442_2024-04-10_143205_575px.png" /></a></p>

<p>Following the earthquake, there was a temporary halt in quotations for both the contract and spot DRAM markets. However, the spot market quotations have already largely resumed, while contract prices have not fully restarted. Notably, Micron and Samsung ceased issuing quotes for mobile DRAM immediately after the earthquake, with no updates provided as of April 8th. In contrast, SK hynix resumed quotations for smartphone customers on the day of the earthquake and proposed more moderate price adjustments for Q2 mobile DRAM.</p>

<p>TrendForce anticipates a seasonal contract price increase for Q2 mobile DRAM of between 3% and 8%. This moderate increase is partly due to SK hynix's more restrained pricing strategy, which is likely to influence overall pricing strategies across the industry. The earthquake's impact on server DRAM primarily affected Micron's advanced fabrication nodes, potentially leading to a rise in final sale prices for Micron's server DRAM, according to TrendForce. However, the exact direction of future prices remains to be seen.</p>

<p>Meanwhile, DRAM fabs outside of Taiwan have none been directly affected by the quake. This includes Micron's HBM production line in Hiroshima, Japan, and Samsung's and SK hynix's HBM lines in South Korea, all of which are apparently operating with business as usual.</p>

<p>In general, the DRAM industry has shown resilience in the face of the earthquake, with minimal disruptions and a quick recovery. The abundant inventory levels for DDR4 and DDR5, coupled with weak demand, suggest that any slight price elevations caused by the earthquake are expected to normalize quickly. The only potential outlier here is DDR3, which is nearing the end of its commercial lifetime and production is already decreasing.</p>

</p> Memory&body=https://compbuddey.blogspot.com/2024/04/report-impact-of-taiwanese-earthquake.html){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

0 Comments